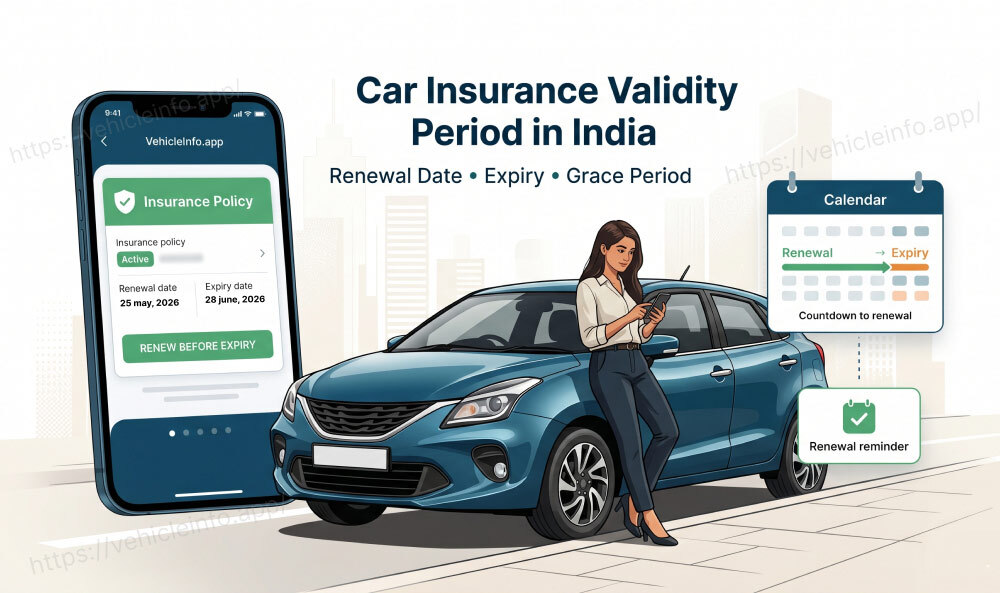

Car Insurance Validity Period in India: Renewal Date, Expiry and Grace Period

25 June, 2026

A car insurance policy carries a fixed shelf life, and the day it ends, your legal cover ends with it. Most private car policies run for one year on the own-damage side, after which they expire on a set date and must be renewed to stay valid. Miss that date, and your car is uninsured from the very next morning, exposed to fines and full liability for any accident.

The confusion usually starts with the word grace. Owners assume a buffer exists after expiry that keeps them covered. It does not, at least not in the way most people think. The rules that the car insurance validity India framework sets are precise, fixed partly by the Motor Vehicles Act and partly by the insurance regulator, and getting them wrong can cost you both money and legal standing.

How Long Is a Car Insurance Policy Valid? Standard vs Long-Term

The car insurance validity period depends on the type of cover. A standard private car policy is usually valid for one year, after which it must be renewed. Thus, for those wondering how long is a car insurance policy valid in India for most owners, the definitive answer is twelve months from the start date.

A comprehensive policy covers both third-party liability and your own car, with the own-damage portion almost always annual. So the practical answer to how long is car insurance valid is one year for a standard policy. New cars are the exception and follow a longer rule covered later, so always check your policy schedule for the exact start and expiry dates.

IRDAI Rules on Policy Year and Renewal Date

The insurance regulator sets the rules that govern your policy year and renewal. A motor policy is generally valid for one year and must be renewed before the due date. Insurers must send timely renewal reminders, but the legal duty to renew on time rests with you. The renewal date is the day after your policy expires, and renewal must be completed on or before the expiry date to keep cover unbroken.

Recent regulatory updates also brought more flexibility on policy duration, with insurers now able to offer terms of less than a year, a standard year, or longer. But whatever the term, the car insurance validity India rules require active, unbroken cover, with the renewal landing before expiry to maintain it.

What Is a Grace Period for Car Insurance? Does One Exist?

This is the single most misunderstood point in motor insurance. The honest answer to what is the grace period for car insurance renewal is is that no grace period keeps your cover active after expiry. Once the policy expires, you are uninsured, full stop.

What people call a grace period is actually a window for retaining your No Claim Bonus. If you renew within 90 days of expiry, you keep your accumulated NCB discount, but this window does not extend your cover. During those days, your car is uninsured, you can be fined, and any accident leaves you personally liable. The insurance grace period car owners imagine is a discount-protection window, not a cover window.

Short-Term Policies: When Are They Issued?

Short-term car insurance, valid for less than a full year, is issued in specific situations rather than as a general option. Regulatory changes have made flexible durations possible, so insurers can now offer policies spanning less than a year, used in cases like bridging a gap until a longer policy starts or aligning a renewal date with another policy.

For most owners, an annual policy remains the simplest and most common choice. Whatever the term you choose, the cover is only valid for the exact period stated on your policy schedule, and it must be renewed before that period ends.

What Happens the Day Your Policy Expires

The day your policy expires, the protection switches off completely. There is no buffer. From the first day after the expiry date, your car is uninsured in every legal and financial sense.

Three things happen at once. You are driving without valid cover under the Motor Vehicles Act, exposing you to a fine of up to Rs 2,000 for a first offence under Section 196. Your own car loses all protection, so any accident, theft, or fire damage comes out of your own pocket. And if your car injures someone, you personally pay the compensation a court awards.

Break-in Insurance: IRDAI's Process After a Lapse

When you renew after the car insurance expiry date has passed, the insurer treats it as a break-in policy. The most important element is inspection. A policy that has lapsed, even by a single day, usually requires the insurer to inspect the vehicle before issuing fresh cover to confirm its condition after the uninsured gap.

Many insurers now allow this through a mobile app, where photos or a short video stand in for a physical inspection, avoiding the need to drive an uninsured car. A timely renewal, completed before the car insurance expiry, skips inspection entirely.

Long-Term Third-Party Policies for Cars: Validity Rules

New private cars follow a different validity rule for the mandatory portion. Since September 2018, following a Supreme Court direction, new private cars must carry a three-year third-party policy at the time of purchase. The third-party cover is valid for three years, not one, which closes the gap where owners forgot their first renewal and left fresh vehicles uninsured.

The own-damage cover, however, usually remains annual even on a new car. So a new car can have a three-year third-party validity running alongside a one-year own-damage policy that you renew each year, keeping the car insurance validity period complete.

Standalone Own-Damage Policy: Validity and Its Link to Third-Party

A standalone own-damage policy covers only your own car, and its validity is tied to your third-party cover. The rules do not allow an own-damage policy to run longer than the third-party policy backing it, because own-damage cover cannot exist on its own legally. This matters for new car owners who hold a three-year third-party policy and buy a separate annual own-damage cover alongside it.

The practical takeaway is that your two covers can have different validity periods, but they are connected. Letting the third-party portion lapse undermines the own-damage cover too. To keep your full car insurance validity intact, both elements must stay active.

How to Check Your Car Insurance Validity Online

You can confirm your car insurance validity period at any time using official government portals, and it takes under a minute. The simplest route is the VAHAN portal. Log in with your mobile number, enter your car's registration number and the verification code, and the system shows your insurer's name and the validity date. You can also use Parivahan Sewa, the mParivahan app, all of which draw on the same central data.

One caution applies. A newly bought or renewed policy can take a few weeks to appear in these databases. If your record shows blank or expired just after a renewal, the cause is usually a sync delay, not a real lapse. Recheck after a few days and keep your policy document as proof.

Consequences of Letting Validity Lapse

Letting your car insurance validity in India lapse triggers consequences across three fronts at once, and they compound the longer the gap runs.

Legal

The moment your cover lapses, you are driving without insurance under the Motor Vehicles Act. The penalty under Section 196 is up to Rs 2,000 for a first offence and up to Rs 4,000 for a repeat, applied to both driver and owner. At checkpoints, officers verify your status digitally, so an expired record is caught automatically.

Financial

A lapse strips all protection for your own car and exposes you to unlimited liability for harming others. If your car causes injury or death during the gap, you pay the full compensation a court awards. Any damage to your own car is also uncovered.

NCB

If the gap exceeds 90 days, your No Claim Bonus resets to zero, raising your future premium. This quiet cost follows you for years, making a missed car insurance expiry expensive long after the gap closes.

Renewing Before vs After Expiry: What Changes

The single most important decision is whether you renew before or after the expiry date, because the two paths lead to very different outcomes.

| Factor | Renew Before Expiry | Renew After Expiry |

|---|---|---|

| Cover continuity | Unbroken | Gap with no cover |

| Vehicle inspection | Not required | Usually required |

| No Claim Bonus | Retained | Retained only if within 90 days |

| Legal status during gap | Always covered | Uninsured until renewed |

| Renewal speed | Immediate | Slower due to inspection |

Renewing before expiry keeps everything clean. Cover stays continuous, no inspection is needed, your NCB is safe, and you are never uninsured. Renewing after expiry introduces a gap during which you are uninsured, usually triggers an inspection, and risks your NCB if the delay crosses 90 days. The answer to Can car insurance be renewed after expiry in India is yes, but with these costs attached. Treat your renewal date as a fixed deadline and keep your cover unbroken.

Frequently Asked Questions

1. How long is a car insurance policy valid in India?

A standard private car policy is usually valid for one year. The answer to how long is a car insurance policy valid in India is twelve months for most owners, with the own-damage portion renewing annually. New cars carry a three-year third-party validity at purchase.

2. How long is car insurance valid for a new car?

For a new private car, the third-party cover is valid for three years, while the own-damage cover usually remains annual. So, how long is car insurance valid differs by component on a new car.

3. What is the grace period for car insurance renewal?

There is no grace period that keeps the cover active after expiry. What is the grace period for car insurance renewal really refers to the 90-day window for retaining your No Claim Bonus. During that window, your car is still uninsured.

4. Does a grace period for car insurance exist?

Not for cover. The insurance grace period car owners imagine only protects your NCB if you renew within 90 days. The moment the car insurance validity period ends, you are uninsured until you renew.

5. Can car insurance be renewed after expiry in India?

Yes. The answer to Can car insurance be renewed after expiry in India is yes, but it usually requires a vehicle inspection and risks your NCB if the gap exceeds 90 days. You are also uninsured during the gap.

6. What happens on the day my policy expires?

Your cover switches off entirely. From the day after the car insurance expiry, you are driving without insurance, exposed to a fine of up to Rs 2,000, with no protection for your own car and full liability for any harm you cause.

7. How do I check my car insurance validity online?

Use the VAHAN portal, Parivahan Sewa, the mParivahan app, or the IIB portal. Enter your registration number to see your validity date. This confirms your car insurance validity period, though a new policy may take a few weeks to appear online.

8. What is a break-in policy?

A break-in policy is a renewal completed after the car insurance expiry date has passed. It usually requires a vehicle inspection before fresh cover issues, since the insurer must confirm the car's condition after the gap.

9. Does my No Claim Bonus survive a lapse?

Only if you renew within 90 days of expiry. Beyond that, the NCB resets to zero, raising your premium. This is why the car insurance renewal deadline matters even when you eventually renew.

10. Can an own-damage policy run longer than my third-party cover?

No. A standalone own-damage policy cannot exceed the duration of the third-party policy backing it. The own-damage cover must always sit within a valid third-party policy, keeping the two parts of your car insurance validity linked.

11. How soon should I renew before the deadline?

Renew before the car insurance renewal deadline to keep cover unbroken. Acting a few days early avoids any risk of a sync gap or a missed date. A timely renewal needs no inspection and keeps your NCB and legal status intact.

12. Is the renewal date the same as the expiry date?

The renewal date is the day your policy expires, and renewal must be completed on or before it. Treating the car insurance expiry as a hard deadline is the simplest way to keep your validity continuous.