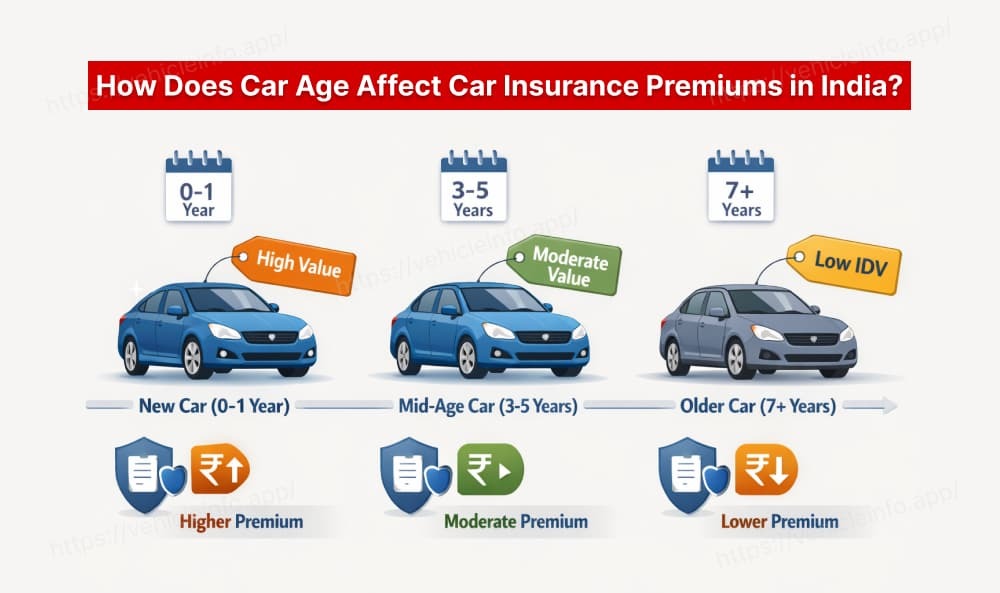

How Does Car Age Affect Car Insurance Premiums in India?

27 January, 2026

When you buy or renew car insurance, insurers consider several factors to calculate the premium-and one of the most important among them is the age of the car. The vehicle’s age directly impacts its value, the type of coverage required, and ultimately the insurance premium you pay.

In simple terms, older cars usually attract lower insurance premiums because their market value declines over time. However, this also affects the level of coverage and claim amount you may receive. Let’s understand this in detail.

How Does Car Age Influence Insurance Premiums?

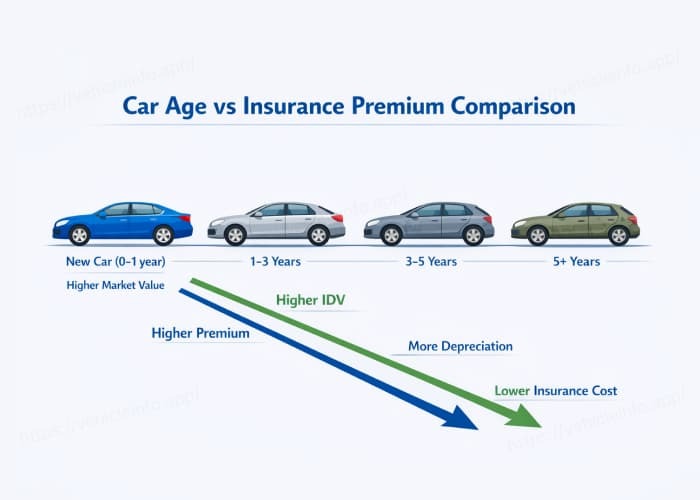

The age of a car plays a crucial role during car insurance renewal. Insurers use the vehicle’s age to calculate its Insured Declared Value (IDV), which represents the maximum amount you can claim in case of total loss or theft.

As a car gets older, its value depreciates due to wear and tear. This depreciation lowers the IDV, which in turn reduces the insurance premium. However, a lower IDV also means a smaller claim payout in case of major damage.

How Is the Age of a Car Calculated?

The age of a car is calculated based on the difference between the calendar year and the model year of the vehicle.

Example: If a car has a model year of 2008, then in the calendar year 2011, the car’s age will be calculated as 4 years (2008, 2009, 2010, and 2011).

How Is Car Insurance Premium Calculated Based on Car Age?

When renewing a car insurance policy, the insurer recalculates the IDV using the car’s age and applicable depreciation. IDV is calculated using the manufacturer’s listed selling price and subtracting depreciation.

IDV Calculation Formula

Insured Declared Value (IDV) = (Manufacturer’s listed price – depreciation) + (cost of accessories – depreciation on accessories)

IRDAI Depreciation Rates for IDV Calculation

The Insurance Regulatory and Development Authority of India (IRDAI) has defined standard depreciation rates used for IDV calculation:

- Up to 6 months - 5%

- 6 months to 1 year - 15%

- 1 to 2 years - 20%

- 2 to 3 years - 30%

- 3 to 4 years - 40%

- 4 to 5 years - 50%

For vehicles older than 5 years, the IDV is decided through mutual agreement between the insurer and the policyholder. In such cases, insurers may rely on vehicle condition reports, dealer assessments, or market surveys.

Does an Older Car Mean Lower Insurance Coverage?

While older cars usually come with lower premiums, it is important to note that third-party insurance is mandatory, regardless of the car’s age. Optional covers like comprehensive insurance, zero depreciation cover, or add-ons may still be beneficial, especially if the vehicle is frequently used.

Even for older cars, having adequate coverage can protect you from unexpected financial burdens due to accidents, theft, or natural disasters.

FAQs

1. What is a No Claim Bonus (NCB) in car insurance?

Ans: No Claim Bonus is a discount offered by insurers for every claim-free year. The discount increases with each consecutive year without a claim and helps reduce the premium significantly.

2. Are cars older than 10 years cheaper to insure?

Ans: Yes, older cars generally have lower premiums due to reduced IDV. However, insurers may limit coverage options or require vehicle inspections for very old cars.

3. Does making an insurance claim reduce the value of a car?

Ans: Filing a claim does not directly reduce the car’s market value, but it can impact your No Claim Bonus and increase future premiums.